What Is Included in a Business Owners Policy (BOP)?

-

Home

-

Business Owners Policy

-

What Is Included in a Business Owners Policy?

What Is Included in a Business Owners Policy?

A Business Owners Policy bundles general liability, property coverage, and business interruption into one package. But many small business owners don't understand what's actually covered until they file a claim. This guide breaks down what's included, common exclusions like flood and cyber damage, who qualifies, and costly mistakes to avoid when choosing coverage.

I sat across from a restaurant owner last month who had been paying for a Business Owners Policy for three years. When a kitchen fire forced him to close for two weeks, he called to file a claim for his lost income. He was shocked to learn his policy didn't cover that loss. Why? Because he'd never added business interruption coverage, even though he thought it came standard.

This happens more often than you'd think. Business owners sign up for a BOP because someone told them they needed one, but they never really understood what they were buying. They assume it covers everything, or they assume it covers nothing beyond the basics. Both assumptions can be expensive mistakes.

A Business Owners Policy is one of the most common insurance products for small businesses, but it's also one of the most misunderstood. This guide breaks down exactly what's included, what's not, and how to know if you're actually covered for the risks your business faces.

What Is a Business Owners Policy?

A Business Owners Policy is a package insurance policy designed for small to medium sized businesses. Think of it like a combo meal at a fast food restaurant. Instead of ordering each item separately, you get several coverages bundled together at a lower price than buying them individually.

The policy typically combines three main types of coverage: general liability protection, commercial property insurance, and business interruption coverage. Some insurers automatically include all three. Others treat business interruption as an optional add on. This is why reading your actual policy matters more than assuming what's in it.

Insurance companies created BOPs to make coverage simpler and more affordable for businesses that don't have complex risks. A retail shop, a small office, or a salon generally faces predictable risks. They need protection if a customer gets hurt on their property. They need coverage if their building or equipment gets damaged. They might need help if they have to close temporarily after a covered loss.

The BOP packages these protections together. You fill out one application, pay one premium, and manage one policy instead of juggling multiple separate policies.

How a BOP Compares to Other Coverage

A Business Owners Policy is most similar to a homeowners insurance policy. Both bundle multiple types of coverage into one package. Your homeowners policy probably includes dwelling coverage, personal liability, and personal property protection. A BOP works the same way for your business.

The difference is what you're protecting. A homeowners policy covers your house and your personal belongings. A BOP covers your business property and your business liability.

Some business owners start out with just a general liability policy. That covers injuries and property damage you cause to others, but it doesn't protect your own stuff. If someone slips in your store, general liability pays for their medical bills and legal costs. But if a storm damages your inventory, you're out of luck with liability only coverage.

A BOP gives you both sides of protection. It covers damage you cause to others and damage to your own business property. This is why many lenders and landlords require a BOP instead of just general liability. They want to know your business can recover if something happens to your physical assets.

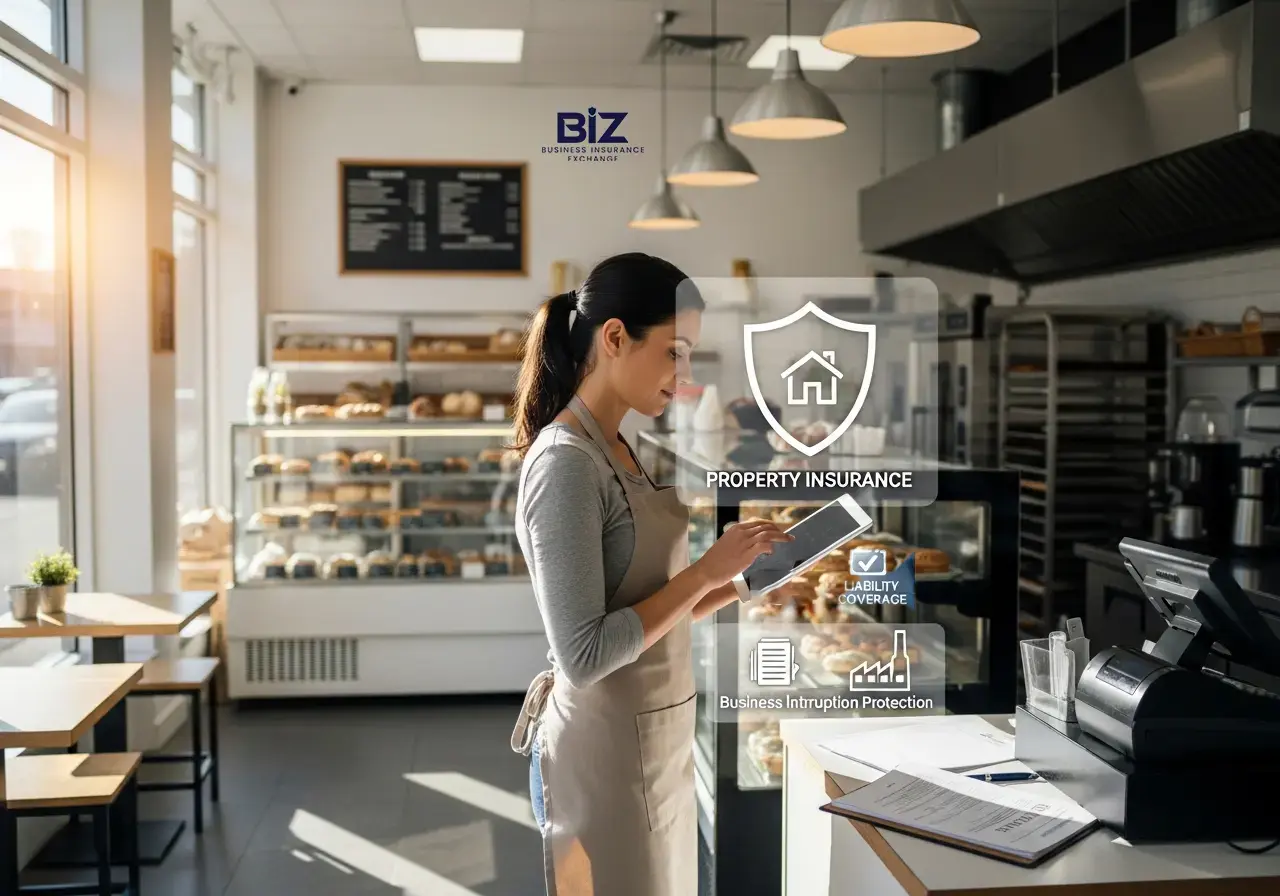

Core Components of a Business Owners Policy

General Liability Coverage

This is the part that protects you when your business causes injury or damage to someone else. If a customer trips over a loose floor tile in your shop and breaks their wrist, general liability covers their medical expenses. If you accidentally damage a client's property while working at their location, it pays for repairs.

General liability also covers advertising injury claims. If someone accuses you of slander or copyright infringement in your marketing, this coverage handles the legal defense.

The typical BOP includes liability limits of $1 million per occurrence and $2 million aggregate. That means the policy pays up to $1 million for any single incident and up to $2 million total during the policy year.

These limits work for many small businesses, but they might not be enough if you work in a high risk industry or handle expensive client property. You can usually increase these limits for an additional premium.

Commercial Property Coverage

This protects the physical assets your business owns or leases. It covers your building if you own it, or your leased space improvements if you rent. It covers equipment, inventory, furniture, computers, and supplies.

If a fire destroys your inventory, commercial property coverage pays to replace it. If a broken pipe floods your office and ruins your computers, the policy covers the cost of new equipment.

Most BOPs also cover outdoor signs, fences, and landscaping up to certain limits. Some include coverage for property in transit, like inventory you're moving between locations.

The coverage typically includes debris removal and the cost of boarding up your property after a covered loss. These expenses add up quickly after a major incident, so having them included matters.

Business Interruption Coverage

This is the part many business owners forget to check for. Business interruption coverage pays for lost income if you have to close or reduce operations due to a covered property loss.

Let's say a storm damages your roof and you have to close for repairs. Your commercial property coverage pays for the roof repairs. Business interruption coverage pays for the income you would have earned during that closure period.

It also covers continuing expenses like rent, loan payments, and employee salaries while you're closed. Without this coverage, you're paying your bills out of pocket while bringing in no revenue.

Not every BOP automatically includes business interruption. Some insurers treat it as an optional endorsement. When you're comparing business owners policy insurance quotes, ask specifically whether business interruption is included or if you need to add it separately.

What Open Perils Coverage Means

Most modern BOPs cover property on an open perils basis, also called all risk coverage. This is better than it sounds.

With open perils coverage, the policy covers any cause of loss unless it's specifically excluded in the policy language. You don't need to check if fire is covered, or wind, or vandalism. If the policy doesn't exclude it, it's covered.

This is the opposite of named perils coverage, which only covers specific risks listed in the policy. Named perils policies might list fire, lightning, windstorm, hail, and a dozen other specific causes. If your loss doesn't match one of those named perils, you have no coverage.

Open perils coverage puts the burden on the insurance company to prove a loss isn't covered, rather than making you prove it is covered. This makes filing claims simpler and reduces disputes over whether a specific cause of loss is included.

But open perils doesn't mean everything is covered. Every policy has exclusions. Understanding those exclusions is just as important as understanding what's included.

What a BOP Doesn't Cover

Insurance policies are known for their exclusions, and BOPs are no exception. Here are the most common gaps you'll find.

Flood Damage

Standard BOPs exclude flood damage. This catches a lot of business owners by surprise. If a storm causes a river to overflow and flood your building, your BOP won't pay for the damage. You need separate flood insurance through the National Flood Insurance Program or a private flood insurer. If your business is in a flood zone, your lender or landlord probably requires this coverage anyway.

Earthquake Damage

Like flood, earthquake damage requires separate coverage. If you're in California or another earthquake prone area, you'll need to add an earthquake endorsement or buy a standalone earthquake policy.

Auto Liability and Physical Damage

If you use vehicles for business, your BOP doesn't cover them. You need commercial auto insurance for liability and physical damage to business vehicles. This includes vehicles you own, vehicles your employees drive for work, and hired or borrowed vehicles. Even if you just use your personal car occasionally for business errands, you should discuss this with your agent. Your personal auto policy might not cover business use.

Professional Errors and Mistakes

A BOP covers bodily injury and property damage, but it doesn't cover professional liability. If you're a consultant, accountant, real estate agent, or other professional who gives advice, you need errors and omissions insurance. If a client claims your advice caused them financial loss, your BOP won't defend you. Professional liability insurance covers these claims.

Employee Injuries

Your BOP doesn't cover injuries to your employees. Workers compensation insurance handles that. Every state has different rules about when you need workers comp, but if you have employees, you almost certainly need it. Some business owners think their general liability will cover an employee who gets hurt on the job. It won't. Workers comp is a separate requirement in virtually every state.

Cyber Attacks and Data Breaches

If hackers steal customer data from your system or ransomware shuts down your computers, your standard BOP won't cover the losses. You need cyber liability insurance for this. Many small business owners assume they're too small to worry about cyber attacks. That's not true. Small businesses are common targets because they often have weaker security than larger companies.

Intentional Damage

If you or your employees intentionally damage property or hurt someone, the policy won't cover it. Insurance covers accidents and negligence, not intentional acts.

Who Qualifies for a Business Owners Policy

BOPs are designed for small to medium sized businesses with relatively low risk. Not every business qualifies. Insurance companies generally offer BOPs to businesses with less than $5 million in annual revenue and fewer than 100 employees. Some insurers have lower thresholds.

The business owners policy requirements also depend on your industry. Retail stores, offices, small restaurants, and service businesses usually qualify easily. Higher risk businesses often can't get a BOP or need a specialized version.

Businesses that typically don't qualify for standard BOPs include:

- Bars and nightclubs

- Auto repair shops

- Manufacturing facilities

- Banks and financial institutions

- Parking lots and garages

If you can't get a standard BOP, you'll need to buy your coverages separately or look for an industry specific package policy.

Your business location also matters. If you operate in a building with certain characteristics, insurers might decline to offer a BOP. Very old buildings, buildings with certain types of wiring or heating systems, or buildings in poor condition can disqualify you.

Optional Coverage You Can Add

Most insurers let you customize your BOP with endorsements and optional coverages. Here are the most common additions.

Equipment Breakdown Coverage

This covers mechanical breakdown of equipment like HVAC systems, refrigeration units, and machinery. If your walk in cooler breaks down and ruins your inventory, equipment breakdown coverage pays for the repairs and the spoiled goods.

Hired and Non Owned Auto Liability

This endorsement covers liability if you or your employees drive vehicles you don't own for business purposes. It's cheaper than full commercial auto insurance but provides important protection.

Employment Practices Liability

This covers claims from employees who accuse you of wrongful termination, discrimination, or harassment. It's separate from workers compensation and covers different types of claims.

Spoilage Coverage

If you store perishable goods and they spoil due to equipment breakdown or power outage, this endorsement covers the loss. Restaurants and food retailers often add this coverage.

Employee Dishonesty Coverage

This covers theft by your employees. If an employee steals cash, inventory, or equipment, this coverage reimburses you for the loss.

Outdoor Property Coverage

The standard BOP has limited coverage for outdoor property. If you have expensive signs, landscaping, or equipment stored outside, you might need higher limits.

How Much Does a BOP Cost?

I get asked about cost constantly, and the answer is always the same: it depends. Business owners' policy insurance costs vary based on your industry, location, revenue, number of employees, claims history, and the coverage limits you choose.

A small office with a few employees might pay $500 to $1,500 per year. A retail store could pay $1,000 to $3,000. A restaurant might pay $2,500 to $5,000 or more.

High risk businesses pay more. Businesses with previous claims pay more. Businesses in areas prone to natural disasters pay more. The coverage limits you select also affect your premium. Higher liability limits and higher property coverage limits increase your cost.

Your deductible matters too. Choosing a higher deductible lowers your premium but means you pay more out of pocket when you have a claim.

To get accurate pricing, you need to request actual quotes based on your specific business details. Generic estimates don't mean much because the rating factors vary so widely.

State Specific Differences

Insurance regulations vary by state, which means BOP coverage can differ depending on where your business operates.

California, for example, has specific requirements around earthquake coverage and workers compensation. If you're shopping for business owners' policy insurance in California, insurers follow different rules than they do in other states.

Some states require certain minimum liability limits. Others have different rules about what can be excluded or how claims are handled.

When you're comparing policies, make sure you're comparing coverage that's actually available in your state. An endorsement offered in one state might not exist in another.

Common Mistakes Business Owners Make

Underestimating Property Values

Business owners often insure their property for less than it would cost to replace. They use the original purchase price or the depreciated value instead of replacement cost. If you paid $20,000 for equipment five years ago, replacing it today might cost $30,000. If you only insured it for $20,000, you're underinsured by $10,000. Always insure property at replacement cost, not actual cash value. Replacement cost pays for brand new equipment. Actual cash value deducts depreciation, leaving you short when you need to replace damaged items.

Assuming Everything Is Covered

Just because you have a BOP doesn't mean every possible loss is covered. Read your policy. Understand the exclusions. Ask your agent about gaps. The restaurant owner I mentioned at the beginning assumed his BOP covered lost income. It didn't, because he never added that coverage. Reading the policy would have prevented that surprise.

Not Updating Coverage When the Business Grows

Your business changes over time. You hire more employees, buy more equipment, increase your revenue. If you don't update your coverage, you might be underinsured. Review your policy annually. Make sure your limits still reflect your current business operations. Tell your agent about major changes like new locations, new services, or expensive new equipment.

Choosing the Cheapest Policy Without Comparing Coverage

The lowest quote isn't always the best deal. One policy might have higher limits, lower deductibles, or better endorsements than another policy that costs less. When you compare business owners policy insurance quotes, compare the actual coverage details. Look at the limits, exclusions, deductibles, and included endorsements. The cheapest policy might save you money now but cost you much more if you have a claim.

Not Reading the Policy

Most business owners never read their insurance policy. They trust their agent to give them the right coverage and never look at the actual contract. Your policy is a legal contract. It tells you exactly what is and isn't covered. If you don't read it, you won't know if you have gaps until you file a claim and get denied. You don't need to become an insurance expert, but you should at least review the declarations page and the exclusions section. This tells you your limits and the major gaps in coverage.

Frequently Asked Questions

A BOP typically covers general liability for injuries and property damage you cause to others, commercial property coverage for your building and contents, and often business interruption coverage for lost income after a covered loss. The specific coverages depend on your policy and any endorsements you add.

No. General liability is one component of a BOP. A BOP also includes property coverage and potentially business interruption coverage. General liability alone only covers injuries and property damage you cause to third parties, not damage to your own business property.

It depends on your business activities. If you meet with clients at your home, store inventory there, or have expensive business equipment, you probably need a BOP. Your homeowners insurance likely excludes business related claims.

Yes, but you might pay higher premiums than an established business. Insurers see new businesses as higher risk because they have no track record. Some insurers specialize in coverage for startups and new businesses.

Commercial property insurance only covers your building and contents. A BOP includes property coverage plus general liability and potentially business interruption. A BOP gives you broader protection in one package.

No. You need commercial auto insurance for vehicles. A BOP might include some coverage for hired or non owned auto liability if you add that endorsement, but it doesn't cover vehicles you own.

At least annually, and whenever you make major business changes. If you hire employees, move locations, add services, or buy expensive equipment, contact your agent to update your coverage.

Final Thoughts

A Business Owners Policy gives small businesses essential protection in a convenient package, but it's not a one size fits all solution. What a business owner's policy includes depends on the specific policy form your insurer uses and the endorsements you select. The biggest mistake you can make is assuming you're covered without actually checking your policy. The second biggest mistake is buying based only on price without understanding what you're getting.

Take time to understand your coverage. Ask questions. Read your policy. Make sure your limits match your actual business assets and risks. The money you save by choosing the cheapest policy won't matter if you discover major coverage gaps after a loss.

Insurance is one of those things you hope you never need to use, but when you do need it, you want it to actually work. Making sure you have the right coverage now prevents financial disaster later. Read more

Related Posts

Not sure if you need a BOP or general liability? Learn the real difference, what each covers, and wh...

Consultants face real legal risks from bad advice claims, missed deadlines, and contract disputes. L...

Get a straight forward explanation of how a Business Owners Policy protects New York business owners...